One of the most overlooked things in personal finance is tracking net worth. When people hear this, they think this is only for the rich and not for everyone. This is a huge misconception because your net worth matters whether you are rich or not. You have to know how much you are spending and how much you are earning and break them down.

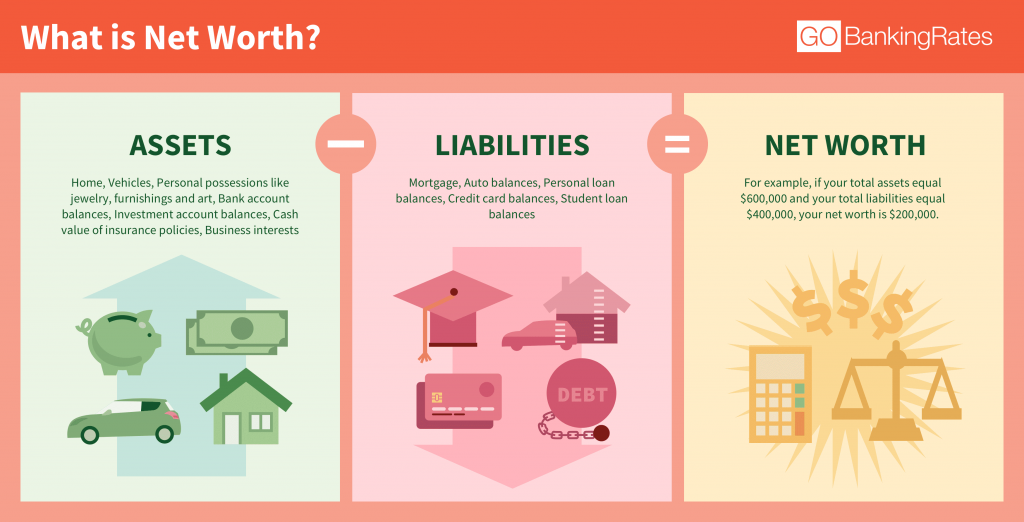

That’s why net worth is the most significant financial indicator to watch. It takes precedence over a person’s wage or monthly budget. Why? It is a simplified representation of your complete financial life in a few numbers. It displays all of your assets accumulated over your lifetime. Net worth also displays all of your current debts. Your net worth is the difference between the two.

To truly grasp the significance of net worth, consider how it relates to a monthly budget. For most people, revenue comes in, and costs send out each month. Those who make more money than they spend add the difference to their net worth. The difference could mean more money in a savings or retirement account. Alternatively, you can use the difference to repay credit cards, school, auto, or other loans. In either case, net worth increases.

When people spend more than they earn, the discrepancy reduces their net worth. It could lead to a reduction in savings or an increase in credit card debt. Again, the net value decreases in either case. The point is that net worth serves as a financial scorecard. It displays your daily and monthly progress on a large scale. It is also quite simple to track.

What is Net Worth Actually?

A net worth tracker is a list of assets and liabilities. Good net worth should just fit on a single page for most people. To track your net worth, you simply need to make two decisions. One, what should be in the net worth statement, and the second, what tools, if any, you should use. Let’s have a look at both of them.

It is not required to add every asset you own to track your finances. All of your personal financial accounts (e.g., checking, savings, investments, and retirement) should be in your net worth. Real estate and businesses must be there, too, if you have any. Your debts are a part of your net worth whether you want them or not. Many people include the worth of their vehicles in their calculations. This is partly to offset the impact of car loans. Even though you can add the liabilities that depreciate, this might not be the best call.

There are exceptions to adding liabilities/properties. That is real estate and businesses. But you have to be careful when valuing them. Most assets are simple to value. Some use Zillow’s estimate for real estate. Some don’t value it all the time, just occasionally check the markets.

How Do You Track Your Net Worth?

The main question that pops up in people’s minds is how. How exactly can you track your net worth? This is both an easy and a tricky question. There are various means to do this. Because we are living in a digital age, there are endless opportunities.

You can choose to use an app that automatically sees all of your money in your bank accounts and transactions. Also, adding your assets there will give you a net worth tracker. There are several automatic tools available to track your net worth. Mint and Personal Capital trackers are two extremely popular options.

These choices not only keep track of your net worth. They also serve as fantastic tools for appraising assets and managing your budget. You may also use Personal Capital to track the value of the real estate by connecting directly to Zillow. Yet, they might not be the most optimal solution. I believe there is a better option.

The option that I prefer over everything is a manual spreadsheet. A basic Google Sheets spreadsheet is an excellent tool for keeping track of your net worth. Sure, it might be a lot of work and needs constant updates, but it gives you the best results.

There are options if you don’t want to waste a lot of time trying to find the ultimate template. You can get various free templates by making a simple Google search. Once you get your template in order, then you can start filling it in. Updating it once a week is generally the best option.

How to Calculate

You determine net worth by deducting all obligations from all assets. An asset is everything that has monetary value that you own. But liabilities are obligations. They drain your resources, such as loans, accounts payable (AP), and mortgages.

Net worth can be positive or negative. The former indicates that assets outweigh liabilities. The latter indicates that liabilities exceed assets. A positive net worth that is increasing implies healthy financial health. On the other hand, declining net worth is cause for concern because it may indicate a reduction in assets relative to liabilities.

The most effective approach to increasing net worth is to either cut liabilities while assets remain constant or grow assets while liabilities remain constant or fall. If you have liabilities bigger than your assets and income combined, you will be in the negative. Having a negative net worth means that you have no money at all. You are losing money every minute you spend like that.

How to Evaluate it Once You Start Tracking it?

Keeping track of your net worth is only the first step. It is also necessary to evaluate the results on a regular basis. Monitoring the change in your net worth over time is an important way to evaluate the results. But knowing what to look for when evaluating is what makes it important.

There are numerous essential financial objectives. Common financial goals include paying debt, saving for retirement, and purchasing a home. Measuring your net worth’s changeover time combines all of these objectives into a single, simple indicator. If you are using a spreadsheet to track your net worth, making a chart showing your growth is as simple as creating a chart.

It’s also critical to consider your net worth in relation to your salary and age. A net worth of $1 million is amazing for a middle-aged teacher, but not so much if you’re LeBron James. Using ratios is a quick and straightforward technique to conduct this assessment.

Charles Ferrell popularized the topic in one of his books. The book explains how much one should and has saved based on income and age. The numbers might change from person to person and from goal to goal. But they might give you a good idea of where you stand.

According to Ferrell, to be on pace for retirement, you should have saved 1.4 times your income by age 35. In other words, someone earning $75,000 a year at age 35 should have $105,000 saved for retirement.

When to Update Your Net Worth

You should ideally update your net worth weekly or monthly. If your net worth includes transactions, the best is to do it weekly. Any longer you go than a month, you risk missing out on precisely measuring your progress. It also affects the understanding of how minor changes affect the big picture. If you do it sooner than weekly, you’ll probably drive yourself insane.

By waiting a month, you ensure that minor changes like your electricity bill don’t fluctuate your net worth. Furthermore, you get your mortgage and vehicle loan statements once a month. So it makes sense to simply wait.

Some people update their net worth statement only once or twice a year. This can work and is preferable to not tracking anything at all. But, it makes knowing where you are over the year challenging. If you have certain objectives in mind, assessing them is critical. To see whether you’re on track or if you need to make modifications to your financial strategy.

How Does It Help Your Financial Freedom?

There are many things a net worth does. Help you to see your situation better and clearer, for starters. It gives you the biggest advantage in your finances. Let’s dive into how tracking your net worth help your financial freedom.

Good Measurement for Your Progress

Calculating and tracking your net worth may be a great source of inspiration. Hopefully, you have a long-term net worth target in mind before retiring. Tracking your net worth allows you to see how you’re doing. If you’re not moving quickly enough, you’ll notice and have time to act and solve the situation.

You can always get motivation. But tracking your net worth will show you that you are on target. It will give you more reasons to keep going and increase the pace.

You See How Your Assets Work For You

It’s always good to look at your net worth and see that it’s increased significantly. Simply because your investments are performing well. It might be difficult to watch as the value of your investments declines. However, these circumstances highlight the significance of your investment selections. How you invest and manage your money is as crucial, if not more so, than how much you earn.

It is worthwhile to devote time to learning about your money and investments. You’ll feel more at ease. You won’t need to hire an expensive financial advisor. In addition, you will get rewarded with a higher net worth over time.

Helps with Better Handling of Money

Tracking your net worth can help you make smarter financial decisions. If you know you’ll be measuring and tracking your net worth in the future, that concept will be in the back of your mind. Especially when you’re tempted to make a poor financial decision.

You definitely care about your financial health if you are making an effort to track your net worth. Your concern will work in your favor. Because you will want to see progress. This will inspire you to make decisions that will save you money and boost your net worth.

Net Worth FAQs

Is there a “good” net worth?

Determining what a “good” net worth is will differ from person to person. It depends on their life circumstances, financial demands, and lifestyle. According to the most recent data from Federal Reserve, the average net worth of an individual in the United States in 2019 was $121,700.

Do you need a specific calculation for net worth?

No. All you need to do is to know how much you have in cash, assets, and liabilities. The only thing you need to have or do is to follow these and know every penny that comes and goes. Knowing these lets you use the formula we mentioned above to get your net worth. It is actually a simple mathematic formula that you see everywhere, even in schools.

Don’t try to go for weird calculations or something entirely different. Even for businesses that are worth billions of dollars, the formula is the same. You just need to have the variables of your finances. Once you have them, you can do it easily.

Is net worth anything special, or can anyone do it?

Net worth is important to anyone that is dealing with money. This could be a business or an individual. Even students could and should follow their net worth. The main point of net worth is not to know how much you are worth. It is mainly to see where you are spending your money and where your money is.

This way, it gets easier to keep track of your transactions. Then you can gradually move towards achieving your financial goals. Because you know everything about the money comes in and goes out.