Cash was once king. People used cash or cheques (which are essentially identical to cash) for everyday expenses. They reserved credit card usage for big and rare expenditures – that is if they got credit cards from the banks at all. However, virtually everywhere accepts credit cards nowadays, and some individuals never carry cash at all.

Many personal professsionals in the finance industry spend a lot of time and effort attempting to keep us from credit card. That’s actually for a good reason. Many of us abuse credit cards and wind ourselves in debt. However, contrary to common assumptions, if you can handle plastic responsibly, you’re far better off paying with a credit card than a debit card and limiting your cash expenditures.

Using and having credit cards doesn’t really imply incurring debt. Spend your money properly, pay your balance in full each month, and you’ll gain all the advantages of credit cards without carrying debt or paying interest. Let’s see why you should use a credit card and how often should you use your credit card.

Why Credit Card?

Should you lose your wallet or get mugged, any cash you have with you is very probably gone forever. However, you will normally not be held liable if criminals use your credit cards to make fraudulent purchases. Cleaning up the mess may take a little time, but you will not lose any money.

Credit card benefits are there to persuade you to use your credit card, and they are quite convincing. You may receive cash back around 1.5 or 2 percent of each dollar you spend with a basic credit card that pays the same amount on every transaction. That is either as a direct credit card cash or as points or even miles to redeem for travel or other goods.

Credit vs. Debit Card

Credit and debit cards are essentially identical in appearance. They have 16-digit card details, expiry dates, magnet stripes, and EMV processors. With one major distinction, both may make it simple and simple to purchase things in shops or online. Debit cards let you spend cash by relying on funds in your bank account. These cards enable you to borrow funds from the card provider up to a specific limit in order to buy the things you wish or withdraw cash.

:max_bytes(150000):strip_icc()/dotdash-050214-credit-vs-debit-cards-which-better-v2-02f37e6f74944e5689f9aa7c1468b62b.jpg)

You most likely have one credit and one debit card in your wallet. They provide unrivaled convenience and security, but there are significant distinctions that might significantly impact your wallet. The biggest reason why financial professors always say to stay away from credit cards is the reason that you spend money you don’t have. If your limit is high, you can get into significant debt that you can’t possibly repay. With debit cards, you can’t spend if you don’t have money.

Advantages and Disadvantages

Advantages

- Credit card use appears on your credit history. This covers both good and negative information. Such as on-time purchases and low credit usage percentages, as well as missed payments or loan defaults.

-

Some credit cards may also give supplementary guarantees or protection on bought products. That is in addition to those provided by the shop or brand. For example, if a credit card-purchased item becomes damaged after the manufacturer’s warranty has ended, it is good to check with the card’s issuer to see whether coverage is available.

- There is a limitation for purchases made after being stolen that you are responsible for as long as the client notifies the loss or theft in a timely way.

Disadvantages

- Using a credit card to make a purchase means you are spending the bank’s money instead of your own. This amount must be reimbursed, together with interest. You must at the very least pay the minimum amount for your debt due each month. Having big balances on many cards might make it tough to keep up with monthly payments and put a strain on your budget.

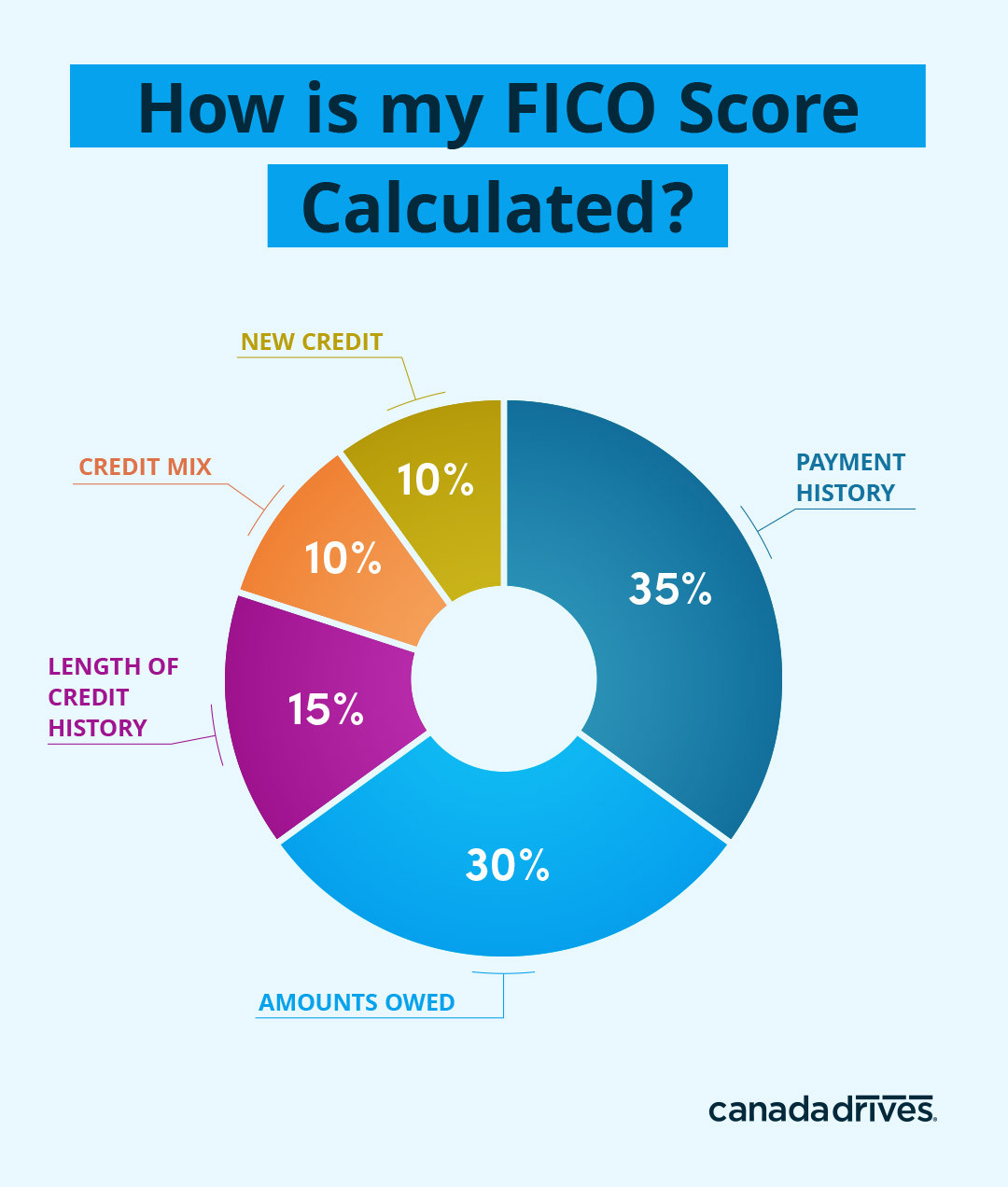

- Paying your debts on time and keeping your card balances low will improve your FICO ratings. However, if you fall into the practice of paying the card debts late, maxing out one or more of your cards, closing older accounts, or applying for new credit too frequently to pay for other loans, you may harm your credit history.

- Since a credit card is really a short-term debt, you’ll have to pay the interest on every transaction you make. Your annual interest percentage rate is calculated using the interest rate and costs charged by the credit business (APR). The greater the APR on the card, the more it will cost you to carry a balance month after month.

The Effect on Your Credit Score

To have good credit, you don’t need a credit card, and you certainly don’t need to carry a debt. However, smart use of these cards is the most effective way to enhance your credit ratings. It makes it simpler to obtain accommodation. Whether a potential landlord is verifying your credit before handing over the keys or you are asking for a mortgage to purchase a property. Cell phone companies and insurance companies may analyze your credit history to determine eligibility and even charges. A good credit score may even improve your chances of being hired, as many firms do credit checks on job applications.

If you have a credit card, make regular little purchases, keep your balance low, and pay your payments on time. This helps to improve your credit score over time without too much hassle. This will put a positive stance on your credit score. Besides, that is perhaps the biggest differentiator in increasing your credit score if you can manage the payments on time.

Is Having a Credit Card Bad?

Credit cards are neither beneficial nor harmful. They are financial instruments that must you must use with caution. Cards can assist or hinder your money, depending on how you use them. Running up debt, skipping card payments, carrying a balance and accruing interest charges, and using excessively of your spending limit are all risks.

In addition, when used correctly, credit cards provide a handy payment mechanism that can help improve credit. Using it responsibly entails just using it for what you can manage to pay off. If you want to prevent trouble, try your best to settle your card bills on time and in full, or as much as you can manage to pay to avoid costly interest charges.

How Bad is Credit Card Debt?

Debt has a bad image, especially when connected with credit cards. Credit card debt is often the costliest type of debt to incur. Credit card interest rates are routinely in the double digits and frequently exceed 20% – even for persons with strong credit. In comparison, the best interest rates for student loans, mortgages, and personal loans can be considerably below 10%. Therefore, if at all possible, avoid putting high costs like medical debt on credit cards. There might be considerably less expensive alternatives.

Read out the “minimum promissory note” on your credit card bill if you want to chuckle — or be scared. It informs you how many years and months you’ll need to repay your credit card debt if you simply make the minimum payment. Assume you owe $8,000 on a credit card with an 18% interest rate and a minimum payment of $160. If you only can afford the minimum monthly payment, you will not be able to pay off the entire credit card debt for seven years, and the seven months and interest you have to pay will be close to the principal amount you owe.

It is also a good rule of thumb to keep a balance between your income and the payments you make. It is undesirable to find yourself in a scenario where the monthly payment for your credit cards exceeds 10% of your usual monthly income. In addition to your credit debt, your credit score must also be in consideration to determine if credit card debt is bad for you right now.

Conclusion

The amount of credit card debt that is detrimental to your credit score is determined by your credit limitations. One of the most important elements influencing your credit score is the quantity of debt you have. When you have zero debt or owe a small amount in comparison to your credit limit, it shows the financial institutions that you can handle credit responsibly and that your credit score will not suffer. However, if you carry an amount that exceeds 30% of your credit limit, your credit score will suffer.